Rising wildfire risk drives up WA home insurance costs

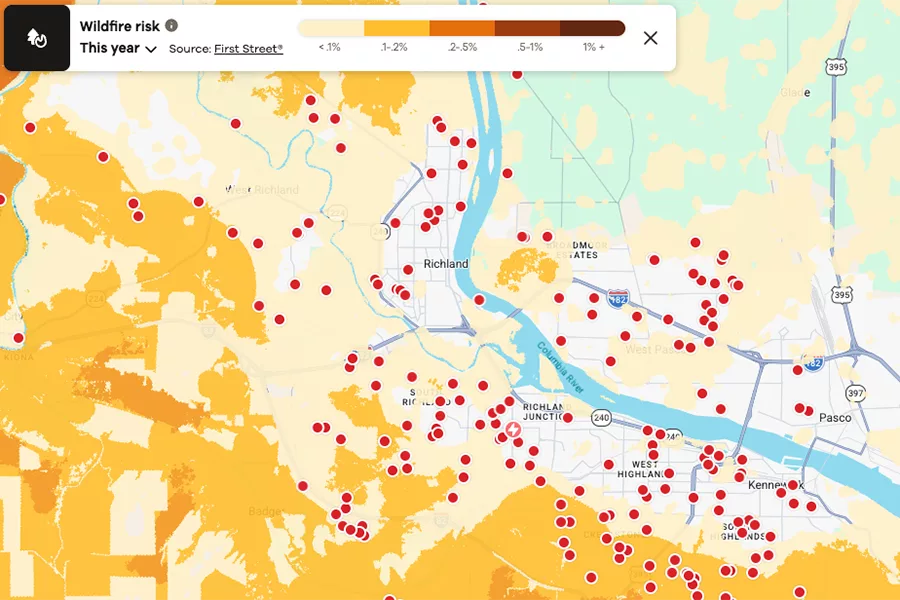

In Benton County, about 73% of all properties are at major risk of wildfires over the next 30 years, according to data from First Street Foundation. In Franklin County, 45% of properties are at moderate risk. Homebuyers can assess homes for wildfire risk on Realtors.com using First Street Foundation’s data.

Courtesy Realtors.comWildfire season is upon us and while you’re thinking about cutting back flammable brush from your home, you also need to make sure your checking account can handle the increased cost to insure it.

Insurify, a national insurance broker, estimates annual property insurance costs in the state will climb 4% on average by the end of 2026, hitting $1,600. That’s on par with the national average, which is being driven by the increasing number of natural disasters, such as wildfires, occurring in recent years.

In Franklin County, home insurance premiums increased by 70% between 2018 and 2024, with Benton County premiums growing just over 50% during that time, according to data from the Washington Center for Real Estate Research.

Some in the insurance and housing industries note the state continues to fare better in premium costs than many other parts of the country, such as Texas or Florida. But that is small succor to the growing number of Washington homeowners who are paying more for coverage or just scrambling to get on a policy.

Busy fire season ahead

The National Interagency Fire Center’s latest wildfire forecast issued June 1 indicates the Mid-Columbia should expect a busy season. May was abnormally warm and dry, despite a few brief rain showers, exacerbating the current drought.

“Significant fire potential is expected to increase across the Northwest Geographic Area during June,” according to the forecast, adding that fire activity in the eastern part of the state will “shift to above normal as live fuels cure, dead fuels dry, and early snow water equivalent (SWE) loss exposes high‑elevation fuels ahead of schedule.”

The Tri-Cities already has had one major fire this season. The Country Meadows fire scorched 1,700 acres in Badger Canyon in May and led to the loss of a shop building. Details on whether any structures sustained any other damage has not been released.

In Benton County, about 73% of all properties are at major risk of wildfires over the next 30 years, according to data from First Street Foundation. In Franklin County, 45% of properties are at moderate risk.

Homebuyers can assess homes for wildfire risk on Realtors.com using First Street Foundation’s data.

Evaluating risk

The increasing rate and severity of natural disasters, including wildfires, is putting the pinch on insurers. Destroyed and damaged homes cost more to replace and repair as the price of building materials continues to climb.

“Severe weather risks are changing how insurers price and structure their policies,” according to a release from Insurify. “To minimize their claims exposure and mitigate further premium increases, insurers are shaping policies to shift more financial risk to homeowners.”

In Washington state, that’s included dropping individual insurance policies. The number of Washington homeowners who have been nonrenewed or canceled by their insurance company, largely due to their home’s wildfire risk, has doubled since 2021, according to the state Office of the Insurance Commissioner.

Two bills supported by state Insurance Commissioner Patty Kuderer and considered by state lawmakers earlier this year sought to bring greater transparency to how insurers evaluate wildfire risk. Neither made it to the governor’s desk.

Review coverage

While premiums have gone up and likely will continue to do so, impacts aren’t being evenly felt by all homeowners. While rural areas saw the largest hikes in premiums between 2018-24, urban counties saw theirs climb as little as 12% during that same period.

“While increasing wildfire risk is affecting the cost and availability of hazard insurance in some parts of the state, Washington has generally not experienced the large average increases in premiums that have occurred in other parts of the country,” wrote Steven C. Bourassa, director of the Washington Center for Real Estate Research.

Regardless, industry officials and experts stress that homeowners review their coverage to make sure they are well protected and minimize the risk that any payout will be inadequate to cover your property losses.

And for need tips on how to protect your home from wildfires beyond cutting back flammable vegetation near your home, go to: bit.ly/nifc-home.